Are you a contractor looking for the right insurance coverage? Getting a clear and accurate contractor policy coverage quote is essential to protect your business from unexpected risks.

But with so many options out there, how do you know what coverage fits your needs without paying too much? This article will guide you step-by-step, helping you understand the key types of insurance every contractor should consider and how to get a quote that works for you.

Keep reading to take control of your coverage and secure your peace of mind today.

Types Of Contractor Insurance

Commercial General Liability covers injuries and property damage caused by your work. It protects against claims from clients or others on site.

Workers Compensation and Employers Liability pay for medical costs if your employees get hurt on the job. It also covers legal costs if employees sue.

Automobile Liability Coverage protects your vehicles used for work. It covers damage or injuries caused by your trucks or cars.

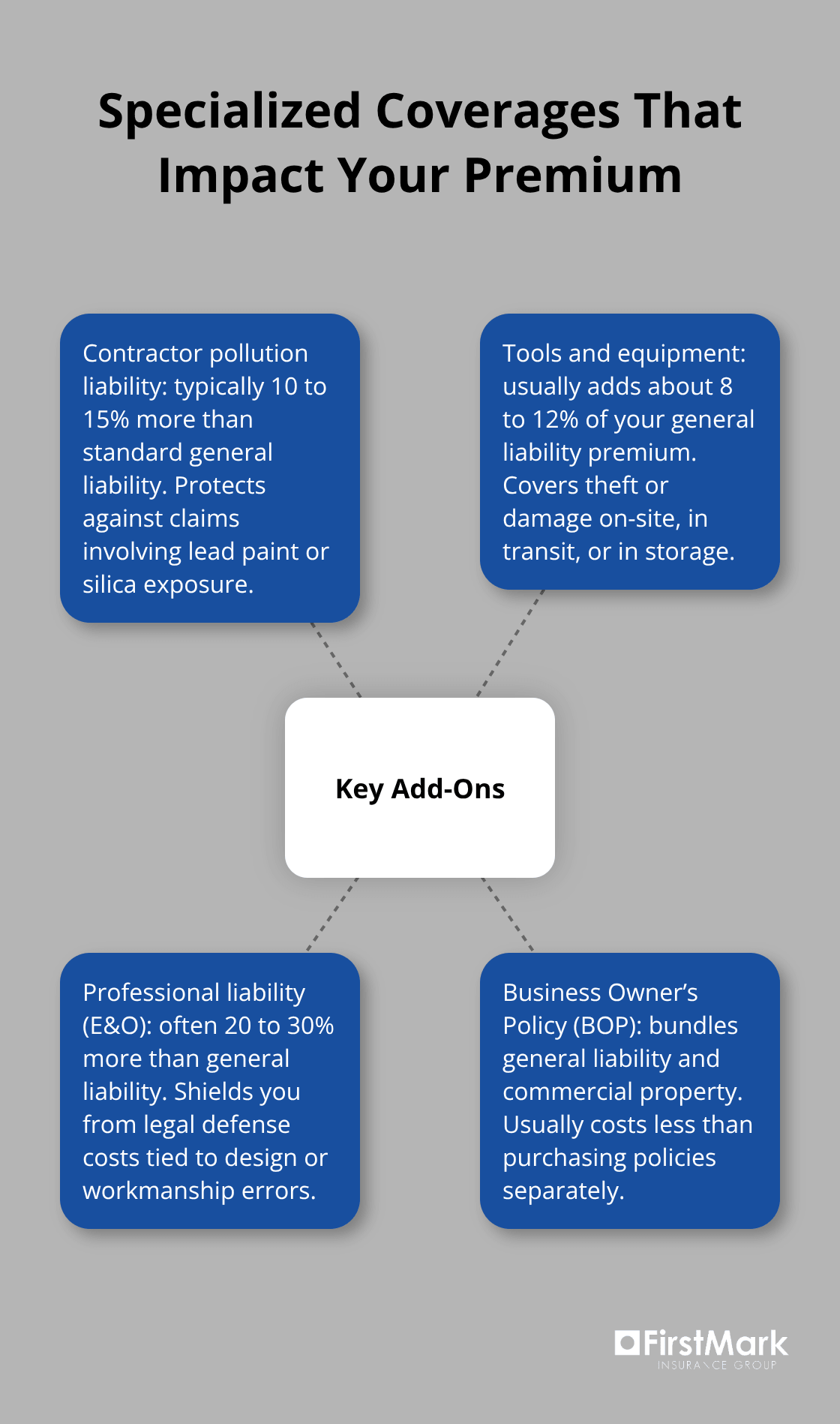

Professional Liability Insurance guards against mistakes in design or advice. It helps pay for legal fees and settlements if clients claim errors.

Builder’s Risk Insurance covers buildings under construction. It protects materials and structures from damage or theft during the project.

Excess and Umbrella Policies add extra coverage above basic limits. They help cover large claims that exceed other policy limits.

Factors Affecting Insurance Quotes

Business size and revenue impact insurance costs. Larger businesses often pay more due to higher risks. Smaller firms may get lower quotes.

Type of contracting work matters. High-risk jobs like roofing cost more to insure than office-based work. The nature of the work affects coverage needs.

Claims history shows your past insurance claims. A clean record can lower your premium. Multiple claims raise red flags and increase costs.

Coverage limits and deductibles determine your out-of-pocket costs. Higher limits mean better protection but higher premiums. Choosing a higher deductible usually lowers your quote.

Location and regulatory requirements also affect prices. States and cities have different rules. Areas with more construction risks often face higher insurance rates.

How To Compare Contractor Insurance Quotes

Compare coverage options carefully to meet your needs. Check what each policy covers and excludes. Some policies may not include certain risks.

Understand policy exclusions to avoid surprises. Know what is not covered, like specific job types or damages.

Look at the insurer’s reputation. Choose companies known for paying claims fairly and on time. Read reviews and ratings from other contractors.

Assess customer service quality. Quick, clear help matters when filing claims or asking questions. A good insurer supports you well.

Use online quote tools to compare prices fast. Enter your details once and get multiple quotes. It saves time and shows options side by side.

Tips For Lowering Insurance Costs

Bundling multiple policies can lower insurance costs by giving discounts. Buying general liability and workers’ comp together saves money. Many insurers offer better rates for bundled coverage.

Implementing safety programs helps reduce accidents and claims. Training workers to follow safety rules lowers risks. Safer workplaces often mean lower premiums from insurers.

Maintaining a good claims record shows you manage risks well. Few or no claims over time can lead to discounts. Insurers reward contractors who keep claims low.

Choosing higher deductibles lowers monthly premiums. Be sure you can pay the deductible if a claim happens. This option helps save money but needs careful planning.

Regularly reviewing and updating coverage ensures you only pay for what you need. Adjust coverage as your business grows or changes. This keeps costs fair and avoids overpaying.

Where To Get Contractor Insurance Quotes

Direct insurance providers offer quotes quickly, often online. You get policies straight from the company. This can save time and reduce costs.

Insurance brokers and agents help find the best coverage for your needs. They compare many companies and explain options clearly. Brokers work for you, not the insurance company.

Online comparison platforms let you see many quotes in one place. You can easily compare prices and coverage. These sites save effort and help spot the best deals.

Specialized contractor insurance companies focus only on contractor needs. They understand risks and offer tailored policies. These companies may provide better coverage for your trade.

Frequently Asked Questions

How Much Does A $1,000,000 Liability Insurance Policy Cost?

A $1,000,000 liability insurance policy typically costs between $400 and $1,500 annually. Prices vary by industry, location, and risk factors.

What Insurance Coverage Does A Contractor Need?

Contractors need Commercial General Liability, Workers’ Compensation, Automobile Liability, Professional Liability, Builder’s Risk, and sometimes Umbrella insurance. These cover accidents, injuries, property damage, and professional errors.

Is 50/100/50 Good Liability Insurance?

A 50/100/50 liability insurance policy means $50,000 bodily injury per person, $100,000 per accident, and $50,000 property damage. It offers basic coverage but may be insufficient for higher risks or serious claims. Assess your needs and local laws before choosing this limit.

What Are The 4 Types Of Insurance Coverage?

The four types of insurance coverage are health, auto, home, and life insurance. Each protects different risks and assets.

Conclusion

Choosing the right contractor policy coverage starts with getting a clear quote. Quotes help you compare prices and coverage easily. You can protect your business from risks and losses this way. Understanding what each policy covers saves time and money.

Stay informed about the types of insurance you need. This keeps your work and team safe. A good quote makes your decision simpler and smarter. Don’t wait to secure the right coverage for your contracting business.