Have you ever wondered how much it might cost to protect your business from unexpected shutdowns? Your business interruption policy cost can vary, but understanding it is crucial to keeping your company safe when disaster strikes.

Imagine losing income because of a fire, storm, or other events that force you to pause operations—how would you cover your bills and keep your team afloat? You’ll discover what influences the cost of business interruption insurance and how to find the right coverage without breaking the bank.

Keep reading to secure your peace of mind and protect your business’s future.

Business Interruption Policy Basics

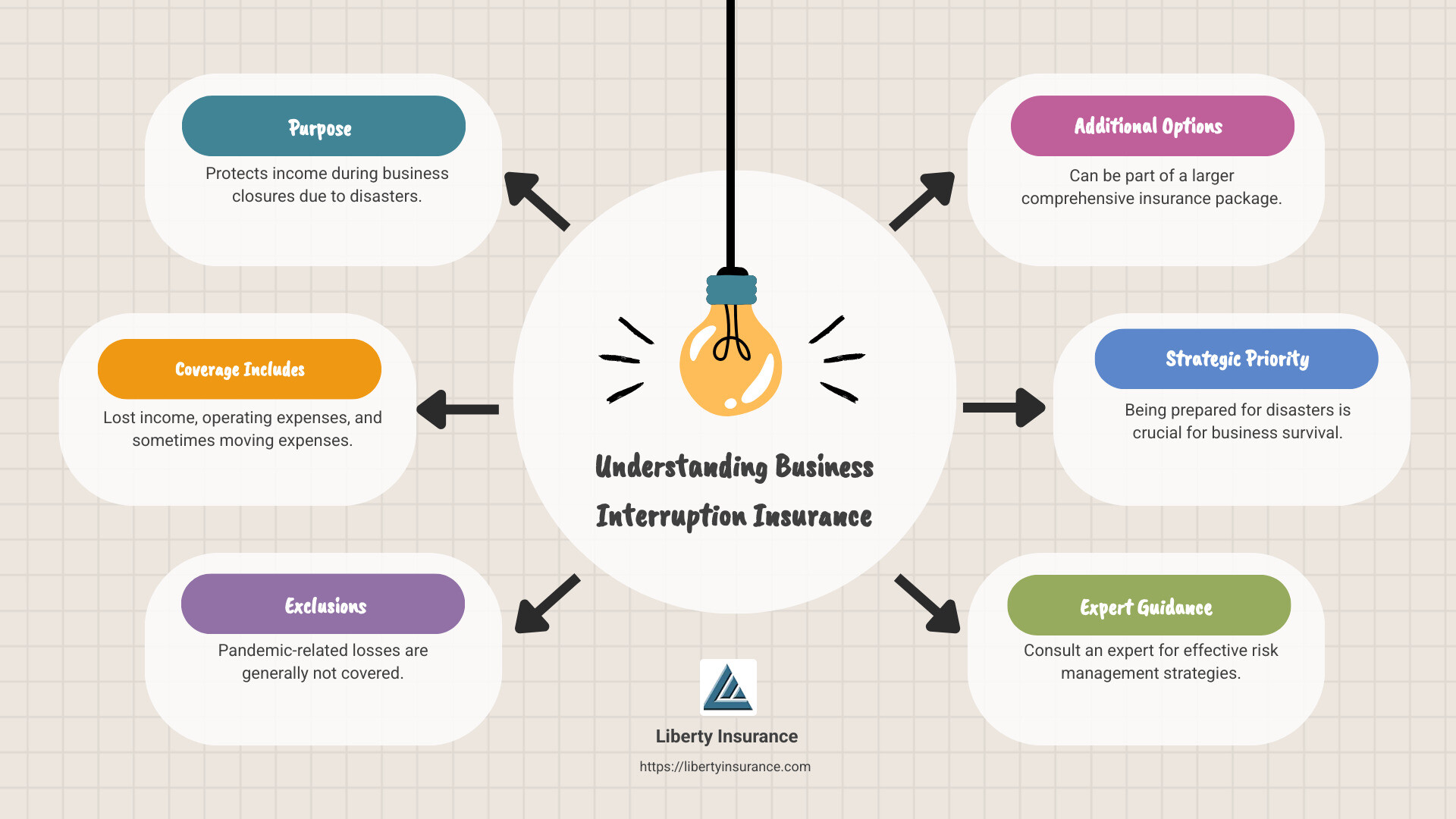

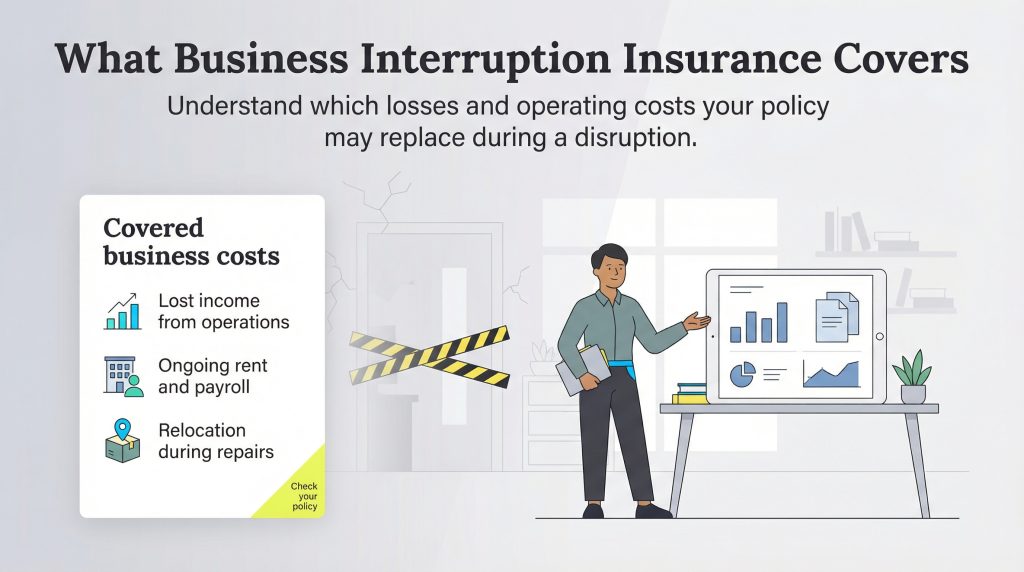

Business interruption insurance helps protect your business from lost income during unexpected closures. It covers lost profits and ongoing expenses such as rent, utilities, and payroll while your business is not operating.

This insurance often applies when damage happens from fires, storms, or other disasters that disrupt normal business activities. It may also cover extra costs to keep your business running or to relocate temporarily.

Key terms include:

- Covered Peril: The event causing the interruption, like fire or flood.

- Waiting Period: The time before coverage starts after a loss.

- Indemnity Period: How long the insurer pays for losses.

- Gross Profit: Income minus variable costs, often used to calculate payouts.

Factors Affecting Policy Cost

Industry type greatly influences the cost of business interruption insurance. High-risk industries often pay more. Location matters too. Businesses in areas prone to natural disasters may face higher rates.

Business size and annual revenue also affect pricing. Larger businesses with higher income usually pay more because their potential losses are greater.

Coverage limits set the maximum amount the insurer will pay. Higher limits mean higher premiums. Deductibles are the amount paid out of pocket before insurance kicks in. Choosing a higher deductible lowers premium costs.

Ways To Lower Your Policy Cost

Choosing the right coverage helps reduce your business interruption policy cost. Select only the coverage that fits your business needs. Avoid paying for extras you don’t need. This keeps your premiums lower and your protection clear.

Improving risk management lowers chances of damage and claims. Maintain your equipment and property regularly. Train employees on safety rules. A safer business means fewer claims and lower insurance costs.

Bundling insurance policies can save money. Many insurers offer discounts if you buy multiple policies together. Combine your business interruption policy with property, liability, or other insurance. Bundling simplifies payments and often cuts overall costs.

Comparing Quotes And Providers

Getting accurate quotes requires clear information about your business. Provide details like industry type, location, and annual revenue. This helps insurers offer precise prices.

Compare providers by looking at their reputation, claim process, and customer reviews. Choose ones with good support and fair claim handling. Don’t pick only by price.

Ask about what the policy covers and exclusions. Some providers offer extra services or faster claim payments. These can add value beyond cost.

Request quotes from multiple insurers to see price differences. Review each offer carefully. Look for hidden fees or limits on coverage.

| Factor | Why It Matters |

|---|---|

| Business Details | Impacts risk level and premium rates |

| Provider Reputation | Affects claim ease and customer trust |

| Coverage Options | Ensures policy fits your needs |

| Price Quotes | Helps find affordable yet adequate coverage |

Common Mistakes To Avoid

Underinsuring your business can lead to big problems. If coverage is too low, you may not get enough money to cover losses. This mistake often leaves business owners struggling to pay bills during downtime.

Ignoring exclusions in your policy causes surprises. Some events or damages may not be covered. Always read the fine print to know what is and isn’t included. This helps avoid denied claims later.

Delaying purchase risks missing protection when needed most. Waiting too long leaves your business vulnerable to losses from unexpected events. Buying a policy early ensures you have coverage before trouble strikes.

Maximizing Protection Without Overspending

Regular policy reviews help keep your coverage up to date. Businesses change and grow. Insurance needs can change too. Checking your policy often ensures you are not underinsured or paying for extra coverage you do not need.

Adjusting coverage as your business grows is important. More employees, higher sales, or new equipment mean higher risks. Increasing your coverage limits can protect your income better. It also helps avoid gaps that cause losses during interruptions.

Review your policy yearly. Talk with your insurance agent about changes in your business. Update your coverage to match your current risks. This saves money and maximizes protection without overspending.

Frequently Asked Questions

How Much Does Business Interruption Insurance Cost?

Business interruption insurance costs vary widely, typically ranging from $500 to $3,000 annually. Pricing depends on industry, business size, location, and coverage amount. Getting multiple quotes helps find the best rate for your specific needs and risk factors.

How Much Does A $1,000,000 Liability Insurance Policy Cost?

A $1,000,000 liability insurance policy typically costs between $400 and $1,500 annually. Prices vary by industry, location, and risk factors.

How Much Does A $1,000,000 Term Life Insurance Policy Cost?

A $1,000,000 term life insurance policy typically costs $20 to $60 monthly. Rates vary by age, health, and term length.

How Much Does A $500,000 Insurance Policy Cost?

A $500,000 life insurance policy typically costs $20 to $60 monthly. Rates vary by age, health, and coverage type.

Conclusion

Choosing the right business interruption policy cost can protect your company’s future. Costs vary based on industry, location, and business size. Understanding these factors helps you pick suitable coverage. Protect your income from unexpected disruptions and stay prepared. Investing in this insurance brings peace of mind during uncertain times.

Review options carefully to find the best fit for your business needs.