When you take out a mortgage, you’re making a big commitment—not just to your home, but to your family’s future. Have you thought about what would happen to your mortgage if something unexpected happened to you?

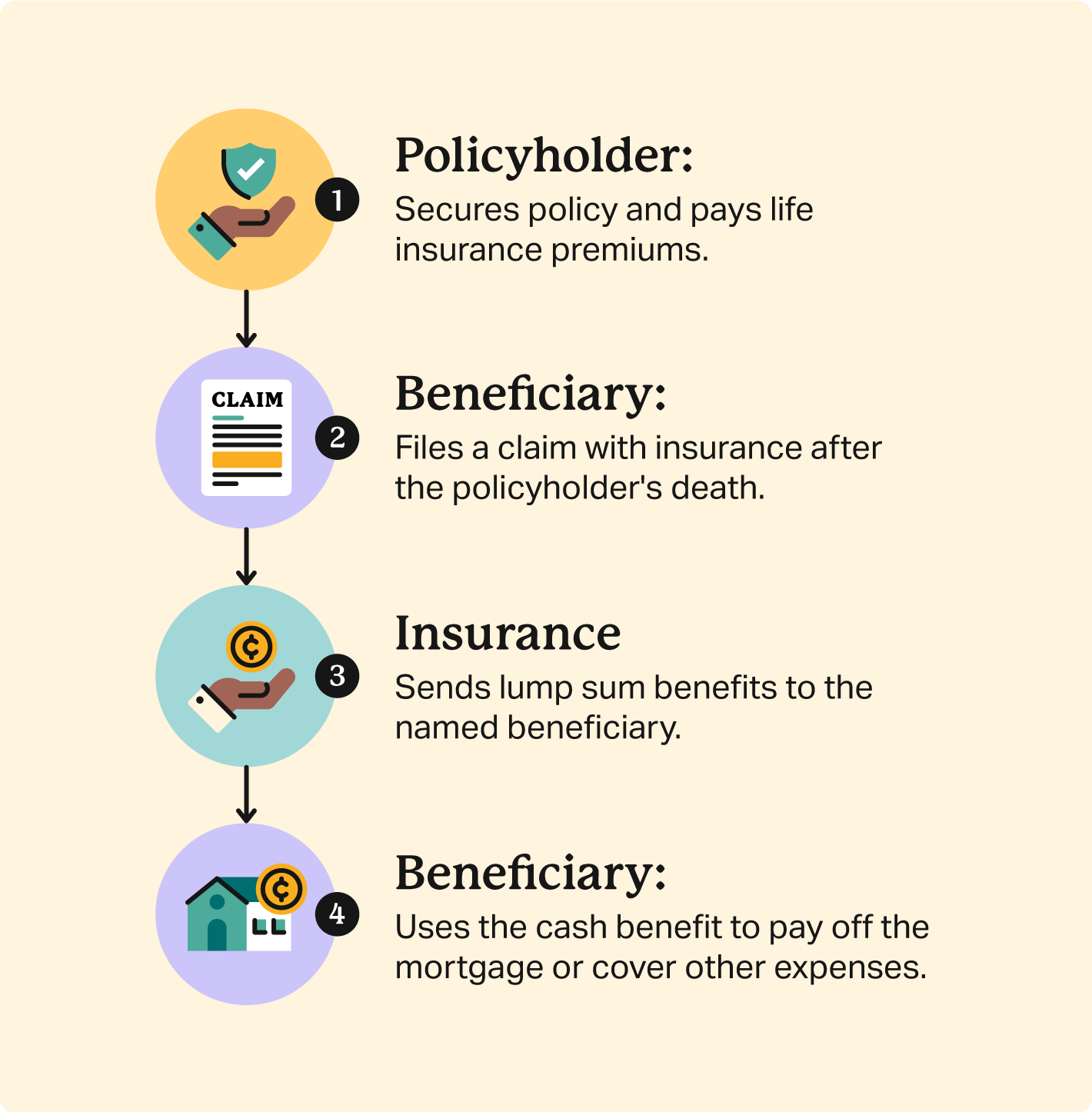

That’s where Mortgage Life Policy Cover comes in. It’s designed to protect you and your loved ones by paying off your mortgage balance if you pass away. Imagine the peace of mind knowing your family can keep their home without worrying about monthly payments.

You’ll discover how Mortgage Life Policy Cover works, whether it’s the right choice for you, and what to consider before making this important decision. Keep reading to find out how you can secure your home and protect your family’s future today.

What Mortgage Life Policy Covers

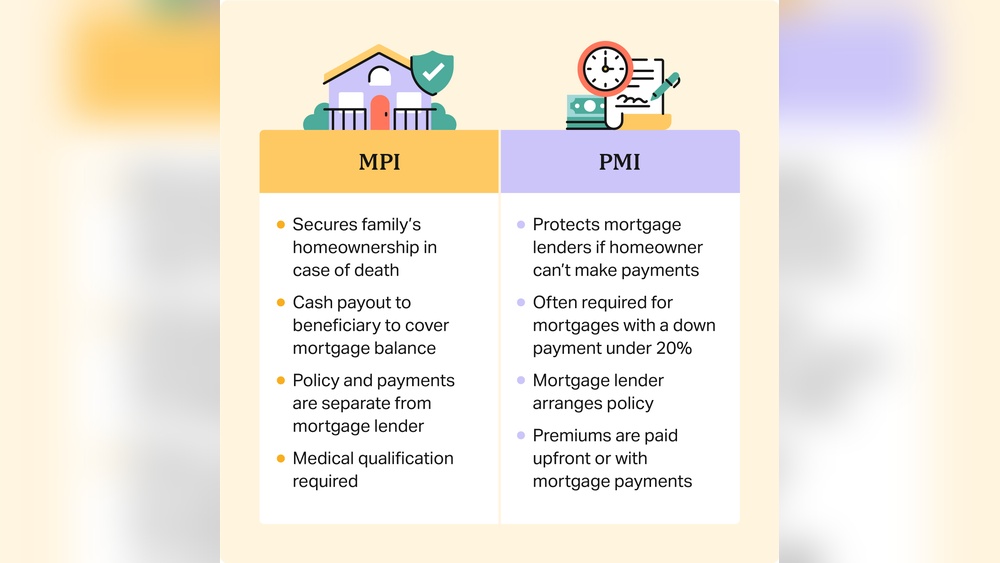

Mortgage Life Policy mainly covers the remaining mortgage balance if the borrower passes away. This means the lender gets paid off, so the family won’t lose the home. It does not pay out cash to family members directly.

Some policies also cover additional expenses like unpaid property taxes, legal fees, or mortgage interest. These can help ease the financial burden during a difficult time.

| Policy Limits | Exclusions |

|---|---|

| Usually covers only the mortgage amount | Does not cover other debts or living expenses |

| Coverage reduces as mortgage is paid down | Excludes death from certain risky activities or illnesses |

Benefits Of Mortgage Life Insurance

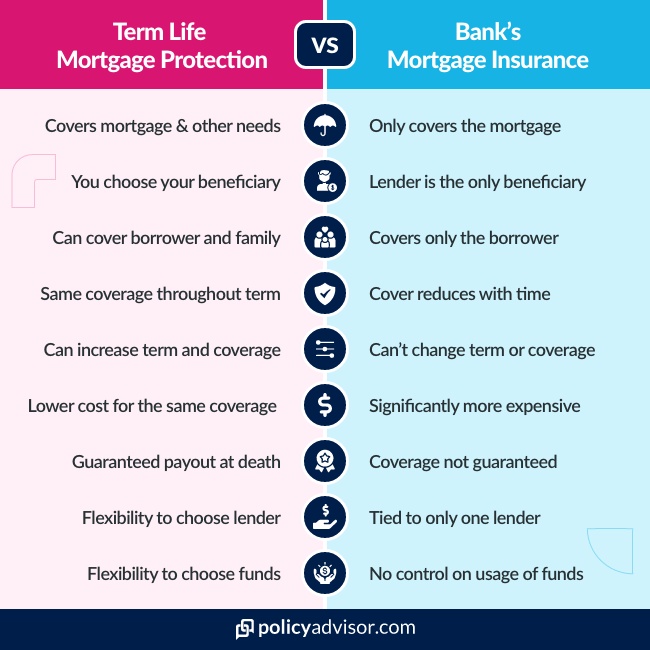

Mortgage life policies usually cost more than traditional life insurance. This is because the coverage only lasts as long as the mortgage does. Traditional life insurance offers more flexibility and may cover other financial needs beyond the mortgage.

Coverage limits in mortgage life policies can be restrictive. The payout decreases as the mortgage balance goes down. This means beneficiaries might receive less money over time compared to a standard life insurance policy.

Beneficiaries might face challenges with mortgage life policies. The payout goes directly to the lender, not the family. This limits how the money can be used, which might not help with other expenses.

Drawbacks To Consider

Decreasing Term Policies reduce coverage as the mortgage balance lowers. The payout shrinks over time, matching the debt. This type is usually cheaper and fits most home loans.

Level Term Policies keep the same coverage amount throughout the term. The payout stays constant even if the mortgage balance drops. This option offers steady protection and peace of mind.

Group Mortgage Insurance is offered by lenders or employers. It covers multiple borrowers under one policy. Usually, it is easier to get but may have less flexibility.

Frequently Asked Questions

What Does Mortgage Life Insurance Cover?

Mortgage life insurance covers your outstanding mortgage balance if you die during the policy term. It ensures your family can pay off the home loan.

How Much Is Pmi Insurance On A $300,000 Home?

PMI on a $300,000 home typically costs 0. 5% to 1% annually. Expect $1,500 to $3,000 per year. Rates vary by lender and credit score.

Is It Worth It To Get Mortgage Life Insurance?

Mortgage life insurance can be worth it if you want to ensure your mortgage is paid off after death. It protects your family from financial burden and secures their home. Evaluate costs and coverage to decide if it fits your needs and budget.

Can I Get Life Insurance If I Have Cirrhosis?

Yes, life insurance is possible with cirrhosis but options may be limited. Expect higher premiums or coverage restrictions. Applying early improves chances. Consulting specialized insurers can help find suitable policies.

Conclusion

Choosing mortgage life policy cover offers peace of mind. It ensures your mortgage is paid if you pass away. Your family can stay in the home without financial stress. This type of cover protects your loved ones from losing their home.

Keep coverage simple and affordable to suit your needs. Review your policy regularly to keep it up to date. Protecting your home protects your family’s future too. Consider this option as part of your financial planning today.