Choosing the right life insurance policy can feel overwhelming. You want to protect your loved ones without overpaying or signing up for something that doesn’t fit your needs.

But how do you know which policy is best for you? That’s where comparing life insurance policies comes in. By understanding the key differences between term and permanent life insurance, and by looking closely at coverage, premiums, and benefits, you can find a plan that gives you peace of mind and financial security.

Keep reading to discover simple ways to compare your options and make the choice that’s right for your unique situation. Your family’s future depends on it.

Life Insurance Types

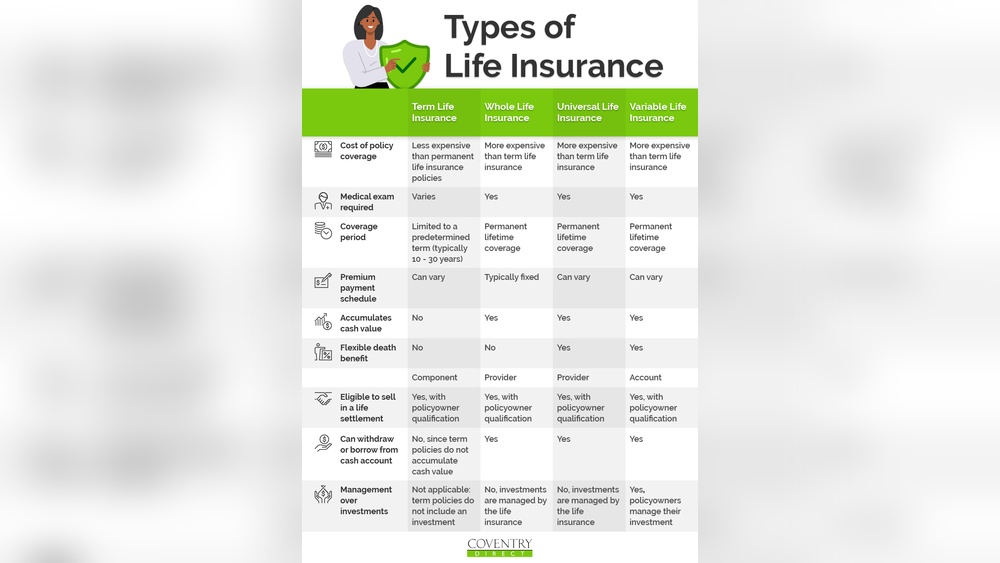

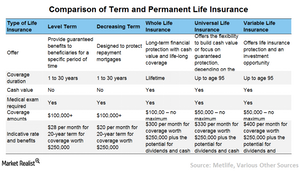

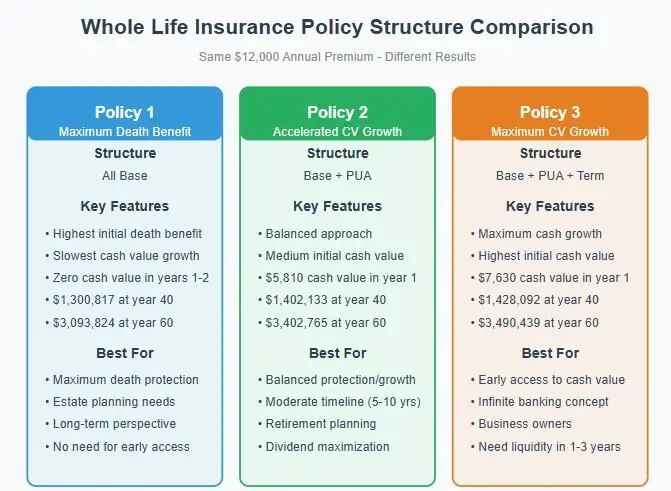

Life insurance has three main types: Term Life, Whole Life, and Universal Life. Term Life offers coverage for a set period, usually 10-30 years. It has the lowest premiums but no cash value. Whole Life covers you for your entire life. It has higher fixed premiums and builds cash value that grows over time. Universal Life also provides lifelong coverage but with flexible premiums. It lets you adjust payments and death benefits. Its cash value depends on market performance, so it can grow more or less. Term Life is best for those needing temporary protection, like covering a mortgage. Whole Life suits people wanting stable premiums and savings. Universal Life fits those who want flexibility in their policy and investment growth.

Coverage And Premiums

Coverage length varies by policy type. Term life insurance covers a set period, like 10, 20, or 30 years. Permanent policies, such as whole or universal life, provide coverage for your entire life. Choosing the right length depends on your financial goals and family needs.

Premium costs differ widely. Term life usually has the lowest premiums because it covers a limited time. Whole life insurance costs more due to lifelong coverage and cash value growth. Universal life offers flexible premiums, which can change based on your payments and policy performance.

| Benefit | Term Life | Whole Life | Universal Life |

|---|---|---|---|

| Coverage Length | Fixed term (10-30 years) | Lifelong | Lifelong |

| Premium Cost | Lowest, fixed | Higher, fixed | Flexible, adjustable |

| Cash Value | None | Guaranteed growth | Market-linked growth |

Choosing The Right Policy

Assessing your needs is the first step in choosing a policy. Think about who depends on your income and what costs they might face without you. Consider debts, daily expenses, and future plans like college or retirement.

Budget considerations are key. Term life insurance often has lower premiums but only covers a set time. Permanent policies cost more but last your whole life and build cash value. Choose what fits your current finances and long-term goals.

Family and estate planning means thinking about how your policy supports your loved ones. Permanent life insurance can help with estate taxes and leaving an inheritance. Term insurance is good for short-term needs like paying off a mortgage or raising kids.

Comparing Life Insurance Quotes

Online marketplaces help compare life insurance quotes quickly. These platforms show prices from many companies in one place. Users can enter their age, coverage amount, and health details to get accurate quotes.

Several factors impact life insurance rates. Age is a major one; younger people usually pay less. Health conditions like diabetes or heart issues raise costs. Smoking or risky hobbies also increase premiums. Insurance companies use these factors to assess risk.

Shopping online saves time and helps find the best price for your needs. Comparing quotes allows better choices for your family’s future. Some sites offer free tools to estimate coverage based on your income and debts.

Policy Features To Consider

Riders and add-ons can improve your life insurance policy. They offer extra coverage for specific needs. Accelerated Death Benefits let you use part of the death benefit early if you get very sick. This helps cover medical bills or other costs.

Waiver of Premium protects your policy if you cannot pay. If you become disabled and cannot work, the insurance company waives your premium payments. Your policy stays active without extra cost during hard times.

These options add value and protection but may increase your premium. Always check if these riders fit your budget and needs before choosing a policy.

Evaluating Insurance Companies

Financial strength ratings show how well a company can pay claims. Agencies like A.M. Best, Moody’s, and Standard & Poor’s give these ratings. Higher ratings mean the company is more reliable and stable.

Company reputation reflects how trusted and respected an insurer is. Look for companies with a long history and positive reviews. A good reputation often means fewer problems with claims and better service.

Customer service matters a lot. Quick responses and clear answers help you feel confident. Check for easy claim processes and friendly support. Good service can make dealing with insurance much easier.

Cost Comparison By Age

Term life insurance rates are generally much lower than whole life premiums. For example, at age 40, term life might cost $25 to $35 monthly, while whole life ranges from $180 to $225. By age 50, term rates rise slightly to $55 to $85, but whole life premiums increase more sharply, from $260 to $315. At age 60, term life costs $150 to $250, whereas whole life often exceeds $450.

The main reason for these differences is that term policies cover a set period, usually 10-30 years, with no cash value. Whole life covers you for life and builds cash value, which raises the cost. Premiums for term life remain fixed and affordable, while whole life premiums are fixed but significantly higher due to the savings element.

| Age | Term Life (Monthly) | Whole Life (Monthly) |

|---|---|---|

| 40 | $25 – $35 | $180 – $225 |

| 50 | $55 – $85 | $260 – $315 |

| 60 | $150 – $250 | $450+ |

Best Practices For Shopping

Using comparison tools helps find the best life insurance deals fast. Many websites show quotes side by side, based on your age, health, and coverage needs. These tools save time and make it easier to see differences between plans.

Reviewing policy details is key before choosing. Pay close attention to coverage limits, premium costs, and any riders that add benefits. Check if the policy has a cash value option or only death benefit coverage.

Updating coverage over time keeps your policy suitable. Life changes like marriage or having children may require more protection. Review your policy every few years and adjust coverage to fit your new situation and budget.

Frequently Asked Questions

What Are The Main Types Of Life Insurance Policies?

The two main types are Term Life and Permanent Life insurance. Term life covers a specific period. Permanent life includes Whole Life and Universal Life, offering lifelong coverage and cash value options.

How Can I Compare Life Insurance Quotes Effectively?

Use online marketplaces like Policygenius or Progressive. Enter your age, coverage needs, and budget to get instant, personalized quotes for easy comparison.

What Factors Affect Life Insurance Premiums?

Age, coverage amount, health condition, and policy type impact premiums. Term policies usually have lower, fixed premiums compared to permanent policies.

What Is The Benefit Of Cash Value In Permanent Life Insurance?

Cash value grows over time and can be borrowed against. Whole Life offers guaranteed cash value, while Universal Life’s value depends on market performance.

Conclusion

Choosing the right life insurance policy takes careful thought. Compare coverage types and costs to fit your needs. Consider term policies for affordable, temporary protection. Permanent policies offer lifelong coverage with cash value benefits. Review company ratings to ensure financial reliability.

Check for riders like accelerated benefits or premium waivers. Use trusted marketplaces to get multiple quotes quickly. Make decisions based on your age, budget, and goals. A well-chosen policy provides peace of mind for you and loved ones. Take time now to find the best life insurance option.

Read More

- Employer Liability Policy Guide: Essential Tips for Protection

- Business Interruption Policy Cost: How to Save Big and Stay Protected

- Contractor Policy Coverage Quote: Get the Best Rates Today!

- Commercial Policy Review Service: Boost Business Compliance Today

- Policy Coverage Gap Analysis: Uncover Risks and Boost Protection

- Custom Insurance Policy Options: Tailored Coverage for You

- Insurance Policy Comparison Tool: Find Best Deals Fast & Easy

- Policy Premium Savings Review: Unlock Hidden Benefits Today

- Affordable Coverage Policy Quote: Unlock Savings Today!

- Private Healthcare Policy Review: Essential Insights for 2026